The Benefits of Working with WTG’s Certified Floodplain Managers

At WTG, we staff Certified Floodplain Managers (CFMs) and invest in their ongoing training in order to produce the industry’s premier flood zone determinations, and deliver expert guidance directly to our clients with every order.

In many cases, it’s the input and guidance of a CFM that can help successfully navigate otherwise frustrating, complicated or costly flood zone issues that are encountered when developing or investing in a property.

What is a Certified Floodplain Manager?

The national Certified Floodplain Manager program was established by The Association of State Floodplain Managers (ASFPM) in order to verify professional competence in floodplain management.

Program certification, and use of the initials “CFM”, requires training, passing a thorough exam and undergoing continuing education to maintain comprehensive floodplain management skills and knowledge.

CFMs In Action

As you may already know, there are a lot of complicated nuances to the world of floodplain management, regulation, risk assessment and documentation. It’s the role of a CFM to understand core aspects of floodplain management, such as the way maps depict the terrain, structures and flood zones; but also to keep abreast of changes in policy and technology in the field.

This specialized work is what ultimately helps provide clarity, guidance and even protection, for homeowners, agents, investors, developers and any individual involved in a real estate transaction.

WTG’s CFM Services: A True-To-Life Example

In cases where elevation needs to be accounted for in assessing flood risk, our CFMs will use an Elevation Certificate (EC) that is provided to us in order to update all official flood-zone related documentation accordingly.

Upon reviewing the provided EC, if we find that the structure is eligible for a LOMA we would then be able to recommend the LOMA (Letter of Map Amendment) process to remove a structure from SFHA (Special Flood Hazard Area) designation, thereby potentially removing a mandatory flood insurance requirement.

As part of this process, when an EC is provided to us, our CFMs perform a calculation of the exact Base Flood Elevation (BFE) of a structure and compare the BFE to the structural elevation.

Many Elevation Certificates already include a BFE, BUT in our experience these values are usually produced by only looking at the Flood Insurance Rate Map, while in most cases the flood profile is needed in order to obtain the correct elevation.

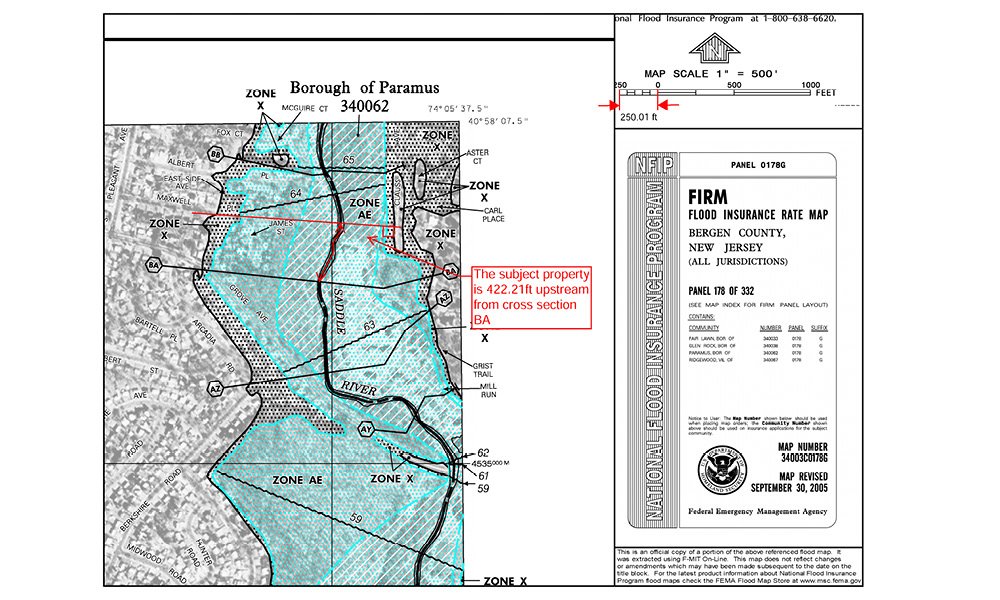

To accurately produce a BFE, our CFM’s will determine the upstream corner of the structure, then create a cross section perpendicular to the direction of flow, and measure the distance from the stream centerline to the nearest cross section.

After that measurement, we will locate the streams Flood Profile found in the counties Flood Insurance Study (FIS). The CFM will then measure the distance either upstream or downstream of the nearest cross section. We can then determine the BFE at the structure's location. A typical analysis is shown below.

Every time we receive an EC we perform this in depth analysis to ensure we provide the most reliable and accurate certified flood zone information.

In the event that the structure is eligible for removal from the SFHA (Special Flood Hazard Area) our CFMs can either submit a traditional LOMA application (6-8 weeks 150.00) or in some situations we can produce an eLOMA (5-10 business days $400.00).

Why Lenders Need CFM Support

Without the expertise of a CFM, the clarity of information on a property can be seriously lacking. This is why many industry-standard 1-page flood reports that are churned out without the hands-on evaluation of a CFM are often misleading, limited, and can even be erroneous.

The best way to get total clarity on a structure’s official flood zone status is to order a certified and insured flood zone determination report from WTG. With each report, you will receive pinpoint accuracy with detailed mapping, insured protection, and expert guidance from our team of highly-trained CFMs.

The information provided is for informative purposes only and is not intended to be legal advice or a legal opinion. For legal advice, please consult an attorney.